Thomas Cangemi came in trying to check at least a couple boxes as the new CEO of New York Community Bancorp: make the company synonymous with more than multifamily lending, and trim funding costs.

Though Flagstar Bancorp in Troy, Mich., may not have been everyone’s first guess as the partner the merger-minded Cangemi would pick, the $2.6 billion deal he unveiled Monday could do the trick in the eyes of the markets.

Shares of the $57.7 billion-asset New York Community, based in Westbury, N.Y., were up over 5% most of the day, and feedback was generally positive for its proposed all-stock purchase of Flagstar.

“This represents a lot of progress all at once,” Janney Montgomery Scott analyst Chris Marinac said. “It’s a timely, strategic deal that makes a lot of sense.”

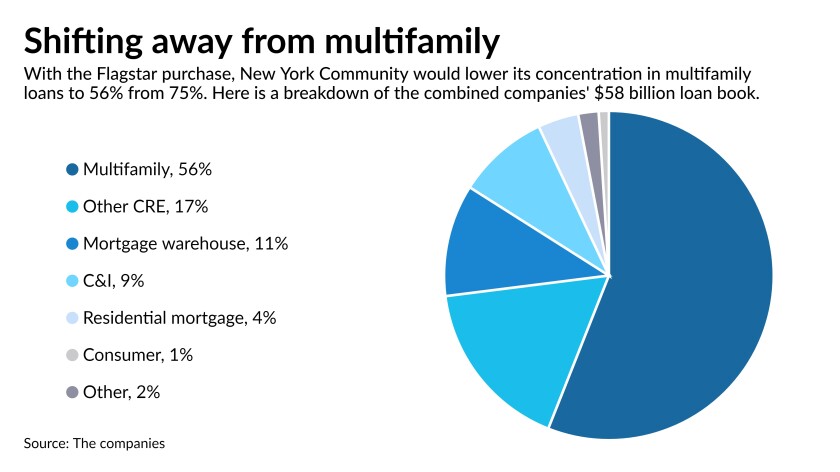

Three-fourths of New York Community’s loan book is concentrated in multifamily, while relatively expensive CDs make up a fifth of its deposits. Its total cost of funds approaches 0.9%, and it also has a high loan-to-deposit ratio of 126%.

With the acquisition of the $29.4 billion-asset Flagstar — slated to be completed in the fourth quarter — New York Community would obtain a sizable national mortgage warehouse business and some residential mortgages. Those additions would lower New York Community’s concentration in multifamily to 56% of the combined company’s total portfolio.

On the other side of the balance sheet, New York Community worried about its interest-rate exposure once rates eventually rise in the coming years. Higher rates on CDs and wholesale funding would drive up funding costs.

Under the deal, CDs would make up 15% of combined deposits, and the total cost of funds would fall to 0.7%. The loan-to-deposit ratio would decline to about 108%, according to a deal presentation. Non-interest-bearing deposits would more than double to 21% of deposits.

“This is a very powerful change in culture,” Cangemi told analysts in a conference call shortly after the agreement was announced. “This is a tremendous step forward."

Wedbush Securities analyst Peter Winter called it a “transformational” deal, highlighting the benefits of a lower-cost funding mix.

“It turns the balance sheet from liability-sensitive to asset-sensitive, which is perfect timing” given that pressure will mount on the Federal Reserve to raise interest rates perhaps as early as next year once the economy gets rolling, Winter said.

Adding other mortgage lines — which would reduce New York Community’s reliance on loans to apartment building owners in places like New York City — “is exactly what they wanted to do,” Winter said.

In addition to diversity, Cangemi said, Flagstar’s mortgage operation and other businesses would help it generate an extra $500 million in capital annually — capital that could support share repurchases, dividend increases or future acquisitions.

However, the mortgage business is volatile. Following a prolonged period of prosperity amid low rates, it is bound to lose momentum in coming years, Winter said. Because of this, he predicted New York Community is likely to pursue further business-line diversity — and potentially more deals — after it digests Flagstar.

Cangemi vowed to pursue acquisitions when he was promoted from finance chief to CEO in January, putting New York Community back in the M&A arena after a decade-long hiatus.

The current environment surely added to the sense of urgency to get a deal done, analysts said. M&A activity is heating up in 2021 — following the pandemic-induced lull of 2020 — as regional banks seek size, efficiencies and both geographic and business-line diversity to compete with the nation’s biggest banks.

“The environment is rich for deals,” Marinac said. “I honestly think it could be merger Monday every week from here on out.”

Seven bank mergers with values over $500 million have been announced this year. In addition to New York Community-Flagstar, two other big combinations have been announced this month alone: BancorpSouth Bank's $2.8 billion proposed purchase of Cadence Bancorp. and Webster Financial's $5.1 billion pending deal for Sterling Bancorp.

In March, Flagstar disclosed in a regulatory filing that it agreed to pay $70 million in cash to fully address a settlement it reached with the government in 2012. The settlement concerned Flagstar’s underwriting practices tied to legacy loans insured by the federal Department of Housing and Urban Development.

Analysts said Flagstar likely resolved that issue to clear the decks for the sale. But on the call with analysts, Flagstar CEO Sandro DiNello emphasized that both companies entered the deal from positions of financial strength.

“Neither of us is a white knight trying to save the other,” he said. “We're both successful and profitable.”

The combined company would have $87 billion of assets, with earning power to grow to $100 billion, Cangemi said. It would have nearly 400 branch locations and 87 loan production offices across the country.

The transaction is expected to be 16% accretive to New York Community’s 2022 earnings per share and 3.5% accretive to its tangible book value per share. The buyer projected cost savings of 11% of Flagstar’s expense base.

The agreement priced Flagstar at 115% of its tangible book value.

“It’s not a big price tag,” Marinac said. “This is much more of a strategic marriage … and the two banks together benefit with growth” that could drive stock appreciation over the long term.

Cangemi would retain his roles as CEO and president, while DiNello will become non-executive chairman. New York Community CFO John Pinto would continue in that role, and the presidents of mortgage and commercial banking at Flagstar — Lee Smith and Reginald Davis — will continue in those roles post-merger.

New York Community would control eight of the company's 12 board seats.

Also on Monday, New York Community reported that its first-quarter earnings available to shareholders rose by 49% from a year earlier, to $137.4 million, or 29 cents a share. Flagstar net income was nearly triple what it reported a year earlier, at $149 million, or $2.80 a share.

Allissa Kline contributed to this article.

"fit" - Google News

April 27, 2021 at 03:20AM

https://ift.tt/3dPGYto

Why New York Community-Flagstar could be a good fit - American Banker

"fit" - Google News

https://ift.tt/2SpPnsd

https://ift.tt/3aP4lys

Bagikan Berita Ini

0 Response to "Why New York Community-Flagstar could be a good fit - American Banker"

Post a Comment